Price Impact and Slippage

When buying or selling through a subnet (liquidity) pool, there is an inherent loss of value during the purchase called Price Impact.

Additionally, there can be unexpected changes to the price (due to other trades, or factors that change the subnet price. This is known as Slippage.

What is Price Impact?

Section titled “What is Price Impact?”Due to the limited resources of the liquidity pool, any change in the ratio of tao/alpha will affect the price and exchange rate. The act of making a purchase through the subnet pool changes the ratio, and affects the rate at which the exchange is placed.

What is Slippage?

Section titled “What is Slippage?”Slippage occurs when additional changes affect the subnet price, and change the amount of tao/alpha received. For example, a transaction may have 0.5% Price Impact but another stake occurs, changing the price, adding a 0.25% Slippage. The entire change is Price Impact + Slippage (in our example (0.75%).

Price Impact & Slippage formulas

Section titled “Price Impact & Slippage formulas”The tao/alpha conversion price cannot be used to calculate a transaction. You must use the following equation to determine the α_received:

The opposite occurs when unstaking alpha to buy tao:

The amount received will be less than the amount expected from the direct price conversion. The difference is denoted as slippage+price impact (generally shown as a percentage):

Price Impact Calculator

Section titled “Price Impact Calculator”Simulate a swap

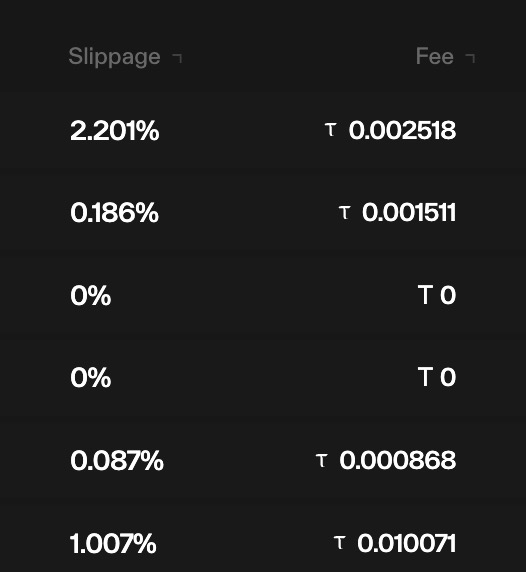

Price impact and Slippage values

Section titled “Price impact and Slippage values”The transaction tables list the actual slippage of a transaction. A negative slippage means your transaction actually profited from the trade